- Ichor share price does not make much sense after performing a discounted cash flow analysis.

- The company is producing some of the most complex subsystems needed by semiconductor manufacturers.

- The stock has already soared this year but we think substantial upside potential remains.

Ichor Holdings (ICHR) has gone up well over 100% for the

year. Despite this the stock still

appears grossly undervalued even if we assume little growth. In reality growth expectations are not low at

all for this semiconductor equipment company.

Recommending stocks after such a strong rally is not generally something

we would consider but Ichor’s current valuation, to be discussed below, makes

us confident that this is still an attractive opportunity for new

investors.

Products

Ichor is a $658 million dollar company involved in the

design and manufacturing of fluid delivery systems for equipment used in

semiconductor manufacturing. The main

products include gas and chemical delivery subsystems which are key components

of tools used in the manufacturing of semiconductors. The gas delivery subsystems deliver, monitor,

and control precise quantities of specialized gases used in semiconductor

manufacturing processes such as etch and disposition. The chemical delivery subsystems blend and

dispense the reactive liquid chemistries used in semiconductor manufacturing

processes such as chemical-mechanical planarization, electroplating, and

cleaning. Finally, the company also

manufactures components for use in fluid delivery systems.

Most semiconductor OEMs outsource the design and manufacture

of their gas delivery subsystems to a few specialized suppliers such as

Ichor. Increasingly OEMs are also

outsourcing the design and engineering of chemical delivery subsystems as a

result of the increased fluid expertise required. Ichor will continue to benefit as this

outsourcing trend continues. The OEMs

benefit by outsourcing the work related to these fluid delivery systems if it

allows them to reduce the fixed costs and development time. In its latest

10K, Ichor says its clients include two of the largest manufacturers of

semiconductor capital equipment in the world, Lam Research (LCRX) and Applied

Materials (AMAT). The company frequently

has its engineers working at its customer’s sites to engage with their product

design teams. This allows the company to

build subsystems to meet the exact specifications of the customer and often

allows them to be the sole supplier of these subsystems during initial

production ramp up.

Company Overview

Ichor has a 17 year history in which it developed deep

capabilities in designing and building gas delivery systems. The company has a global footprint with

facilities located close to its customers.

This has allowed the company to establish long standing

relationships. Over two decades, the company

has been developing complex fluid delivery subsystems to meet the constantly

changing production requirements of semiconductor OEMs. They have significant capacity in Singapore

to support high volume products. The two

companies mentioned previously, Lam Research and Applied Materials, were the

two largest customers by sales in 2016. Sales

from continuing operations grew by an impressive 40% to $405.7 million in 2016

with net income coming in at $20.8 million.

Ichor’s engineering team is made up of chemical, mechanical,

software, and systems engineers. Their

engineering teams work directly with their customers’ product development teams

to provide technical expertise outside their core competencies. The company seeks to use its long standing

relationships with two of the market leaders to locate new business

opportunities created as a result of industry consolidation. The assembly and integration of high purity gas

and chemical delivery systems happens at the company’s locations in Singapore,

Tualatin, Oregon, and Austin, Texas. The

company also has a facility in Malaysia for components used in the gas delivery

subsystems and in Union City, California for components using in chemical

delivery subsystems. These facilities

are located in close proximity to customers.

One of the key elements that make Ichor an attractive

investment is the relatively low rate of capital expenditure. The company is able to grow sales with a low

investment in property, plant and equipment.

The company also highlights its close supplier relationships which allow

it to scale up production quickly without maintaining a lot of excess

inventory. Risk is reduced by this low

fixed cost approach since it minimizes the impact of cyclical downturns on net

income. We prefer this conservative

approach even though it results in a smaller increase in gross margin as a

percentage of sales in times of increased demand.

Fueling Growth

The company acquired Ajax United Patterns and Molds in April

of 2016. This acquisition is what

allowed Ichor to offer chemical delivery subsystem capabilities to its existing

customers. The Ajax acquisition enabled

Ichor to manufacture complex plastic and metal products required by the

medical, biomedical, semiconductor, and data communication equipment

industries. As a result of deploying

more leading edge tools, the company will grow its business as OEMs will need to

refurbish legacy systems.

More recently the company acquired Cal Weld, a leader in

metal component manufacturing which is considered a strategic business for

Ichor. The acquisition cost was $50

million of which $20 million was paid in cash and the rest borrowed. It expands capacity and capabilities in the

component manufacturing area for gas delivery tools in semiconductor

manufacturing. Cal Weld supports key

semiconductor tools such as deposition and etch. The Cal-Weld facilities are located in

Fremont, California and Tualatin, Oregon.

Cal Weld is expected to generate between $65 million to $80 million in

revenue next year.

Source: Ichor

Presentation

While there is currently a risk posed by customer

concentration, the company is seeking to expand its customer base within the

fluid delivery market. The recent annual

report mentions that Ichor was selected as a manufacturing partner for a

provider of etch process equipment that was previously not a customer. The company is also planning to diversify its

sales exposure and leverage its current capabilities by acquiring new products

and solutions for high growth applications in new markets such as medical,

research, and energy.

In the second quarter earnings call the company sounded very

optimistic on continued growth noting that they are seeing increased business

beyond the two largest customers. The company

said its third and fourth largest customers are expected to grow 100% this

fiscal year. One of these customers asked Ichor to redesign their gas delivery

systems for better performance and lower cost.

Risks

Clearly one concern for Ichor is that the semiconductor

equipment OEMs could start developing the gas or chemical delivery subsystems

internally. Otherwise, the primary

competitor is Ultra Clean Technology for gas delivery subsystems. The chemical delivery subsystem industry is

highly fragmented as is the tool refurbishment market.

As a result of the customer concentration issue mentioned

previously, the clients have a significant amount of negotiating leverage which

could lead to price and margin pressure.

Additionally, the company will be impacted by any decline in

semiconductor sales or the various electronic products requiring

semiconductors.

One more unique concern is the fact that Ichor is a largely controlled

by a single investor, Francisco Partners, which owned over 74% of the

outstanding shares at the time of the last annual report. This is a board governance issue since it

means that Francisco basically controls who is elected to the board of

directors which could mean that the interests are not always aligned with the

interests of other shareholders.

Also, keep in mind is that the company is incorporated in

the Cayman Islands and Cayman Islands law provides less protection for

shareholder interests compare to the laws of the United States. Another drawback that comes along with

investing in a company that only recently became public is that there is not the

same level of historical data available as compared with companies that have

been public for an extended period. The

company provides financial statements going back to 2014 which will be

discussed in sections that follow.

Financials & Valuation

The balance sheet is

not ideal given that retained earnings, or in this case accumulated deficit,

are negative and there is some long term debt even if it is not an unreasonable

amount. While there is currently still

an accumulated deficit the value will not be negative for long if the current

pace continues as seen in the table below.

Source: barchart

The current ratio comes in at an acceptable 1.80 and long

term debt to equity stands at 0.22. A

clear positive is seen when looking at the income statement where we see

incredible sales growth in the last three years as well as the last few

quarters. We also like the way the annual

cash flow numbers are looking where cash flow from operations easily covers

capital expenditures and even the 2016 acquisition.

Source: barchart

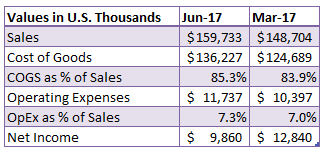

Looking more closely at recent results, it should be noted

that we are seeing some margin pressures.

For the quarter ending in June, although sales increased, net income

actually decreased as a result of increases in the cost of goods sold and

operating expenses. The table below

shows cost of goods sold and operating expenses as a percentage of revenues. One part of the drop in income not shown in

the table is the negative contribution of -$610,000 from discontinued

operations.

Source: barchart

Next, we will take a quick look at our discounted cash flow

model. Rather than use the trailing

twelve month EPS of $3.64, we will use the lower EPS estimate for next year

which is $2.79. We rather use the lower

of the two numbers to keep the model slightly more conservative. The current forward P/E is 9.46. We think this is unreasonably low in

comparison to the industry and market in general and will use a future P/E

ratio of 15 in the model. Finviz provides an optimistic long term EPS estimate

of 29.25%. Earnings did grow by 310% on

a quarter over quarter basis. Keep in

mind that this is at least partially related to the acquisitions mentioned

above. We will not use either of these growth

numbers in our DCF model. Instead we

will adjust the required long term growth rate until the model shows that the

current price is equal to the target buy price.

In this way, we see the growth rate that would be required to get the

return on investment we are looking for.

The DCF model inputs are summarized below:

- · EPS estimate for next year: $2.79

- · Future P/E ratio: 15

- · Discount rate (desired annual return): 10%

- · Long term annual EPS growth rate: 1% (Read notes below)

Again, the long term EPS growth rate used above is not what

we actually expect the growth rate to be.

This is just the calculated growth rate required to make the current

price equal to our target buy price.

Basically, the model is showing us that the stock is grossly undervalued

if one actually believes the analyst estimates or assumes any kind of

substantial growth from here like we do.

Despite the massive run up since the IPO, the DCF model makes us think

there is still plenty of room to the upside.

The table below provides some key valuation and financial metrics for

Ichor.

Source: finviz

Final Thoughts

Clearly the right thing to do was buy the shares at the IPO

price or anytime at the beginning of the year since the stock has already gone

up well over 100% for the year. However,

this does not mean it is too late to initiate a position. In the case of Ichor, we think there is still

plenty of room to the upside from here based on the discounted cash flow model

and growth prospects. We rate Ichor a

buy. Unfortunately, a buy-write strategy

is not a possibility since there are no options available for this stock. Of course, we do not think this is a reason

to ignore Ichor given the significant undervaluation. The potential of this small cap company, with

a market cap of $661.83 million, appears to be going unrecognized by the market

and it may make sense to buy before it starts getting the attention it

deserves. Finally, keep in mind that other

companies in the space like Ultra Clean Holdings (UCTT) trade at much higher

multiples.

No comments:

Post a Comment